The High Cost of Bad Credit

Original Article – https://www.nytimes.com/2023/06/07/magazine/bad-credit-repair.html

Desperate to improve their ratings, Americans now spend billions on “credit repair” — but the industry often can’t deliver on its promises.

By Mya Frazier

- June 7, 2023

When Taqwanna Clark went to buy a video camera at Fry’s Electronics in Houston, she asked if they had a layaway plan. The cashier instead handed her an application for a store credit card. She applied. “Instantly, it came back declined — like, No!” she says. “Denied, denied — you know, your credit is not good enough.” Clark was 30 and working as a security guard at the Port of Houston. On weekends, she performed as a rapper in the local club scene, under the name T-Baby. She wanted the camera to shoot music videos, to promote her music career. “If I can’t afford a $200 camera,” she recalls thinking, “then I’m in a bad way with this credit thing.”

Clark had lived with money anxieties since childhood. In elementary school, her family endured periods of extreme poverty. For a time, on the cusp of homelessness, they lived in the bare framing for a house her father was building on a wooded lot owned by a family member. They slept in an unfinished room and warmed canned food by a fire on a concrete brick. Eventually they moved into a government-subsidized housing complex. In her early 20s, at her mother’s request, Clark says she co-signed a high-interest auto loan on a Dodge Neon for her younger sisters, who never made the final payment. Other missteps followed, like when she let the boyfriend run up a $2,000 bill on her T-Mobile account. When she couldn’t afford the $4,000 needed to repair her car’s transmission, she let the dealer take back the car — unaware at the time that this voluntary repossession would leave her with another debt on her record.

The denial at Fry’s left Clark deflated. After she married the next year, in 2013, she desperately wanted to buy a home. She and her husband, who loaded and unloaded steel pipe for $17 an hour at the Port of Houston, worried about rent increases on their $800-a-month apartment, where they were raising her young daughter. But Clark had watched her mother, during the subprime-mortgage boom, be lured into homeownership by a “teaser” mortgage rate, only to lose her home to foreclosure when that adjustable-rate mortgage ballooned and she could no longer afford the payments. “I didn’t want to do anything that said variable, or A.R.M., or nothing,” Clark says. She applied for preapproval on a fixed-rate mortgage and was denied immediately.

It was only then that she saw her credit history for the first time. It came in the form of a report from one of the many companies that sell reports to mortgage lenders, based on data those companies buy from the three major credit bureaus, Experian, Equifax and TransUnion. The numbers were grim: On the widely used credit-scoring scale, which ranges from 300 to 850, two of her scores were in the low 500s (the third was 700). She stared at the report, befuddled. “I didn’t know there were three companies, with three different scores,” she says. “I didn’t know any of this.” She also didn’t know what exactly she could do.

Clark requested her actual credit reports from the so-called Big 3 bureaus, each of which keeps its own records. Since 2003, the bureaus have been required by law to make these reports available free to consumers once a year. The minutiae of her financial identity were on full display: addresses, employment history, lines of credit, missed payments, collections, closed accounts and credit inquiries from prospective lenders. The $4,552 for emergency dental work her insurance wouldn’t cover. The $2,742 on a Chase credit card she never paid off. But the longstanding T-Mobile debt she had worried so much about was gone. So was the unpaid debt for the Dodge Neon and her own voluntary repossession — after seven years, some negative entries have to be removed from credit reports.

The free reports didn’t include what Clark most wanted to know, however: her credit scores, the credit bureaus’ numerical prediction of how likely someone is to pay back a debt. For those, she had to pay. She signed up for a $19.95 monthly subscription with Equifax, and one day in December 2014, she received her scores. Two were in the mid-500s. “They had this little ‘poor’ underneath them,” she recalls.

Until this point, Clark had paid little attention to the frequent radio ads that she heard on 97.9 the Box, a hip-hop and R.&B. station in Houston, promoting something called credit repair. But when her apartment came under new management, she worried about another rent increase and began looking online for help with her credit. She found seminars that cost as much as $1,500 but settled on two e-books, “Boost Your Credit Score” and “Do It Yourself! Repair Your Credit Now!” which were sold for $20 each on Facebook.

‘Credit scoring reflects, numerically, America’s racial and economic divides.’

By now, Clark had learned about dispute letters. She could send letters to the bureaus challenging the accuracy of entries on her credit report, and if a bureau couldn’t verify the legitimacy of something within 30 days, typically, the bureau was required to delete it from the record. The books included sample letters. Clark chose the most straightforward template:

I am writing to dispute the following information in my file. I have circled the items I dispute on the attached copy of the report I received.

This item [identify item(s) disputed by name of source, such as creditors or tax court, and identify type of item, such as credit account, judgment, etc.] is [inaccurate or incomplete] because [describe what is inaccurate or incomplete and why]. I am requesting that the item be removed [or request another specific change] to correct the information.

Enclosed are copies of [use this sentence if applicable and describe any enclosed documentation, such as payment records and court documents] supporting my position. Please reinvestigate this [these] matter[s] and [delete or correct] the disputed item[s] as soon as possible.

Clark now understood that the best way to repair her credit was to get “deletions.” If she had enough negative items — a late payment, a debt — removed from her credit report, her score might rise.

Over the next couple of years, Clark sent round after round of handwritten letters to the bureaus. To her surprise, she generated some deletions: the unpaid dental bill; the balance she owed on the Chase credit card; and the $110 she owed West Bay Acquisitions, a collection company, for $110 in charges from Black Expressions, a book club she initially paid $1 to join but forgot to cancel. At times she felt uneasy about the process. She wasn’t making good on some of her debts. “The right way to do it would have been to pay it,” she says. But she had learned that even if she paid them, they stayed on her reports, because they had already been sold to a collection agency. “If it’s still going to be on here, what’s the point?”

The deletions weren’t enough. To raise her score to qualify for a mortgage, Clark needed new positive “tradelines.” In the argot of the credit bureaus, tradelines are just another word for all the accounts listed on a credit report — credit cards, loans and mortgages are all tradelines. The e-books included long lists of available secured credit cards, the quickest way for someone to add more tradelines. To obtain these cards, people with low credit scores pay security deposits that can be as much as hundreds of dollars. By taking on additional credit cards, Clark raised her scores to the point where she qualified for a mortgage and a zero-down payment program at a fixed rate, which lessened her fears of losing her home as her mother had. The house that she and her husband bought in Sunnyside, a predominately Black neighborhood in southeast Houston — on a street “people will consider the hood,” Clark says — cost just over $150,000.

Clark was now a zealous advocate for credit repair. “I was running around like a little hummingbird — hey, I know about credit!” she says. She struck up conversations with other Black women in her neighborhood and even gave out her number. “The young girls working at H-E-B, and mothers that were catching a bus, I was like, Let me show you about credit, I’ll fix your credit for free.”

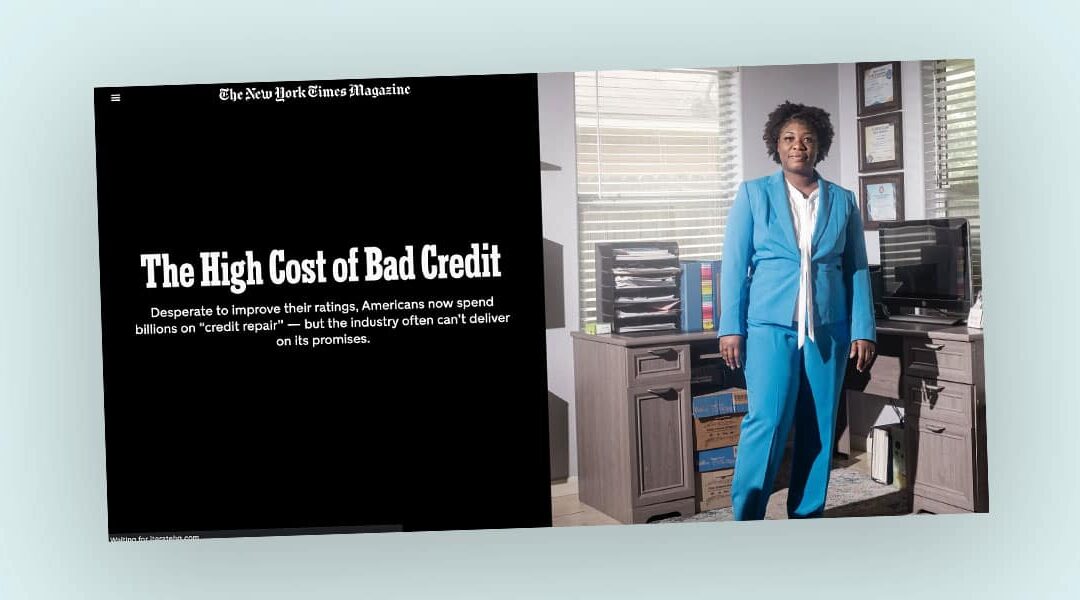

In 2021, Clark opened Credit Lift Inc. She called herself a “credit specialist” and charged enrollment fees ranging from $159 for single clients to $318 for married couples and monthly subscription fees ranging from $120.99 to $201.98. “When people pay, they pay attention,” she says. For those fees, Clark began holding sessions with customers over the phone and on Zoom. She went over each negative item on their reports. Clients sometimes got emotional. The debts could be reminders of difficult times: a lost job, a divorce, a period of homelessness. She would then take on the tedious process of sending dispute letters for them. She charged only after the first round of letters and issued refunds if they didn’t result in deletions.

In starting Credit Lift, Clark had joined the booming business of credit repair. Last year, according to one recent market estimate, the industry had revenues of $4.4 billion, up from $3 billion in 2019. Despite this remarkable scale, many Americans are unaware of the industry’s existence, because the burdens associated with credit break down starkly along racial and class lines. In low-income communities, payment delinquencies on credit cards, mortgages and auto loans — all of which invariably lower credit scores — are twice as high. A report last year from the Federal Reserve indicates that only 11 percent of applicants whose incomes exceed $100,000 said they were turned down (or approved for less than they applied for) on credit applications during a 12-month-period; among those with incomes below $50,000, 43 percent of white applicants and 60 percent of Black applicants were denied credit. (Across all income levels, Black consumers are denied credit more often than their white counterparts.)

The volume of denials, along with the sheer complexity of a credit-reporting system that all but forces people to seek help from others, has spurred the industry’s rise. An estimated 60,000 credit-repair businesses operate independently in the United States, often remotely. (Clark works out of a home office.) Several large firms have managed to establish national footprints, some by creating multilevel-marketing networks of agents, others by selling software programs that include dashboards for analyzing client credit reports or that automate the process of writing dispute letters.

The size of the industry and the depth of the need for credit fixes has also meant opportunity for scams and bad actors. Their stories make the news occasionally. The pastor who, with family and friends, solicited credit-repair clients online, only to rack up charges on credit cards in their names and run up millions in debts. The credit-repair network that functioned as a pyramid scheme by recruiting nearly half a million agents, mostly on social media, with come-ons like, “Who needs negative items removed from their credit report permanently???” The “credit washing” frauds in which credit-repair influencers lodge false claims of identity theft with the police and, often without the knowledge of their clients, submit those police reports as documentation with dispute letters to produce deletions.

Clark was aware of scams like these. As a debtor, she had avoided them herself by sending her own dispute letters. But sometimes she wondered what was the real grift. So much money was sloshing around — and most of it was going to the credit bureaus. Lenders, creditors and collection companies all paid to report negative and positive information to the bureaus; then they paid the bureaus again to get the same information back. Consumers could get their one free report from each bureau each year, but they often had to pay the bureaus, too, if they wanted access to the scores the bureaus were tabulating. “They are selling our information back to us,” Clark told me. “They’re geniuses.”

In many ways, credit scores have become the arbiter of who gets to live the good life in America. A score above 700 opens a world of low-interest car loans, favorable offers to refinance mortgages, a smoother hiring process with employers, the ease of never having to explain away a rough period to secure an apartment. A score below 659 can mean costly consequences. Landlords, and employers in some states, can legally reject applicants because of poor credit; some auto insurers charge as much as 156 percent more in yearly premiums; auto lenders might impose double-digit interest rates.

But the credit score, as we know it today, didn’t even exist until 1989. That’s when Fair, Isaac & Company, a then-obscure data-analytics company in San Rafael, Calif., introduced the now widely used scoring system, which took its name, FICO, from its creator. Today the credit score is so pervasive that even children can get mock credit scores from the app Kiddie Kredit, which, in partnership with Equifax, claims to promote “financial literacy.” In recent years, a flurry of products like Credit Karma, Credit Sesame and Experian Boost have brought the gospel of self-improvement to the management of one’s credit score, something to track and try to manipulate like cholesterol levels or step counts.

Yet the underlying algorithms used to calculate this three-digit distillation of financial identity are hidden; in fact, they are trade secrets, constantly being revised. There isn’t even a single scoring system anymore. In 2006, Experian, Equifax and TransUnion — the Big 3 — introduced the VantageScore to compete with FICO. The Big 3 bureaus surveil every area of people’s financial lives, and the competitive advantage they occupy in the credit system has been described by a Morningstar analyst as akin to having “wide moats” that “can’t be breached.” People’s financial identities are, in effect, the product the bureaus sell, bringing in the bulk of their combined revenues of $15 billion, mostly from fees paid by corporations that want access to their repositories. The “pulls,” through which potential lenders check a consumer’s credit record, number in the billions every year, most of them coming from the largest creditors: banks and their credit-card brands but also auto insurers and lenders, landlords and mobile-phone companies.

Keeping track of who owes what, and what bills are paid on time, has created a dizzying landscape of competing scores and reports. The bureaus each have a somewhat different record of a consumer’s financial history. As a result, we have multiple credit scores, not one; dozens of possible reports, not just three.

A 2021 investigation by Consumer Reports suggests that it’s also a system so prone to error that aspects of the system “appear to be fundamentally broken.” This wasn’t a first-time finding. A study by the Federal Trade Commission, released in 2013, found that one in four consumers identified mistakes on their credit reports that might have lowered their scores. “Credit scores are often unreliable, inaccurate or, in many cases, people won’t even have a credit score,” Rohit Chopra, director of the Consumer Financial Protection Bureau, told an audience of financial technology companies in New York last month. Between 2019 and 2021, the last year for which figures are available, an estimated 335,900,000 items were disputed by consumers, an onslaught the credit bureaus characterize as “industrial scale” and a “flooding.”

With credit-card debt rising faster today than it has in two decades, and household debt at $17 trillion, the stakes are considerable: Payments required on debt loads cost U.S. households $1.75 trillion a year, both cutting into disposable income and, by delivering significant profits to the financial industry, worsening America’s deep economic divides. The situation has created a world of classes based on scores, argue the sociologists Marion Fourcade of the University of California, Berkeley, and Kieran Healy of Duke University. The scoring technologies underpinning the credit-reporting system, they have written, are an “overlooked force that structures individual life chances.” In a 2019 report by the Federal Reserve Bank of Chicago that detailed where people with low credit scores lived across five states, researchers found that households with subprime scores of less than 620 were concentrated in urban neighborhoods with greater proportions of Black residents. Prime households, with scores above 760, were concentrated in disproportionately white suburban areas. As Sara Sternberg Greene, a law professor at Duke University, has written, “Credit scoring reflects, numerically, America’s racial and economic divides.”

Credit repair now closely rivals the individual revenues of the credit bureaus themselves, and this flourishing has come despite the fact that regulators have been vowing to rein it in for decades. It’s an industry of bizarre variability — multilevel-marketing-style organizations, boiler-room operations and by-the-book agents working within onerous federal restrictions on charging fees to customers up front, before any “repair” has occurred — and unequal success. The most successful independent credit-repair agents become millionaires, while others earn little.

‘I bet you a thousand dollars you can’t find me an accurate credit report.’

In recent years on social media, where hanging a proverbial shingle is as easy as coining a clever Instagram handle — creditfixrr, yocredithealer, boostmyscoresnow, mrcredityourself, luxuriouscredit — credit repair has reinvented itself. The ease of targeting people online who have poor credit (“how to fix my credit” is a common search) has both intensified the challenge for regulators and emboldened new forms of grift. “I want to quit credit repair,” Alex Miller, of Alex Miller Credit Repair, told a Texas judge last year, after a Federal Trade Commission investigation alleged that he filed false identity-theft reports to the agency. Miller, who denies the allegation, said at a court proceeding: “I just want to get out of it altogether. I know that once somebody — the government is after you, it’s best just to stop.”

The allure of credit repair as a profession, and its susceptibility to dubious practices, was on display last May, when attorneys, investigators and data specialists from the F.T.C., accompanied by local law enforcement, showed up at the headquarters of Financial Education Services, in the upscale Detroit suburb Farmington Hills. The F.T.C. claimed F.E.S. was running a “sprawling, bogus credit-repair scheme” that promised to significantly improve customers’ credit scores by permanently removing negative information from their credit reports. The company had taken in nearly half a billion dollars in gross revenues, according to federal prosecutors, all of it spent on “worthless credit-repair services,” as the F.T.C. put it. (F.E.S. has denied the allegations.)

F.E.S. had built a network of more than 400,000 credit-repair sales agents across the country. The agents recruited new agents and clients through social media and telemarketing. “If you have 400-675 credit score and want a 700-800 credit score, David can LEGALLY erase negative items … repos, foreclosures, late payments,” one post declared in typical fashion. Another: “My credit score went up 140 points, from a 530 to a 670, in my first 30 days, allowing me to purchase a new home!” Few agents made much of a living, according to an F.T.C. analysis — the average weekly income was just over $2.25, or $117.36 per year. (In one recent year, less than 1 percent of the agents averaged more than $300,000.)

In 2020, as pandemic-era stimulus payments to low-income households created boom times for credit repair, F.E.S.’s customer base rose to nearly 900,000. Revenues soared to $134 million from $73 million the year before, according to court filings. After the F.T.C.’s unannounced visit to the Farmington Hills office, Samuel Levine, the director of the agency’s Bureau of Consumer Protection, vowed in a news release to “continue to pursue firms that prey on families’ economic pain.”

When I first read the F.T.C.’s lengthy complaint, the scale of the operation came as a complete surprise, though I had reported at length on the firm and its business model. A few months earlier, I visited an office storefront run independently by two F.E.S. agents and situated between a community health clinic and a used-car lot on the Near West Side of Chicago. A vinyl banner for the used-car lot next door read, “NO CREDIT BAD CREDIT, WE FINANCE.” Inside, there were colorful upright banners, with GROWTH and WEALTH in block letters arranged sideways. I interviewed a handful of their recruits, including a couple who joined in the hopes of earning enough money to buy a home. After the F.T.C. investigation emerged, they stopped working as F.E.S. agents and declined to be named in this article — “We’d rather not put ourselves out there like that,” one of them told me.

This February, at F.E.S.’s annual convention, held in Orlando, the theme was “Rise,” according to a report by a court-appointed monitor, and an F.E.S. founder, Parimal Naik, presented $100 bills to winners of a “Money Ball” drawing. (Naik declined to comment for this article.) The monitor noted, too, that among the 500 people in attendance, at least 95 percent of the attendees were either Black or Latino.

Matt Liistro, a former mortgage broker who started National Credit Fixers in 1996, is one of the industry’s more vocal promoters. He told me he’s like “an accountant who is trying to get you a loophole and save you money.” He started CreditCon, an annual gathering for the credit-repair industry, six years ago. At this year’s event, held in April in New Orleans, a few dozen booths pitched some product or service to the 300 or so credit-repair agents in attendance. There were booths selling software to automate the creation of dispute letters. There were booths staffed by lawyers looking for referrals that might lead to lawsuits against the credit bureaus.

Some of the busiest booths, I found, were those pitching the sale of the credit-card-payment histories of complete strangers. This was a legal and proven “hack” to increase credit scores, a co-owner of a company running one of these booths told me, next to a tall banner that read, “WHOLESALE AUTHORIZED USER TRADELINES.” It’s legal to add someone, including a nonfamily member, to a credit card as an authorized user. The stranger didn’t get to use the credit card, but the positive payment history — and the length of time the card had been open, a key metric used to calculate a credit score — was factored into the authorized user’s credit report. The vendor I talked to charged roughly $300 to $500 to add each credit card; for someone with bad credit, it might take the addition of several cards, or as much as $1,500, to raise a score.

Jason Moore, dressed casually, circulated among the booths with his tiny brown dog, Ringo. A former subprime auto finance manager from Birmingham, Ala., Moore started TeamUSA Credit Repair and worked his connections among car dealers for referrals after the Great Recession of 2008. “It just blew up so fast,” he told me. “By the third month, I made 30 grand with one employee.” Craig Chapman, a former car salesman, wearing a suit with a pocket square tucked into his jacket, started Transformation Financial Solutions in Dallas after seeing a local dentist — who otherwise seemed to be successful — be turned down for a loan with a credit score of 460. Chapman said, “If she has that problem with credit, how many other millions of people do as well?” Julia King and Robert Longshore, a married couple from Louisville, Ky., had driven their motorcycles to New Orleans from Louisville, where they operate King Financial Repair. They charge new clients $299 for an analysis of their credit reports, then $147 a month thereafter, typically for a minimum of six months. King told me she obtained deletions for clients all the time: wrong dates, incorrect balances, inaccurate dates of when an account was opened or closed. “Something’s going to be wrong every single account,” she told me. “I bet you a thousand dollars you can’t find me an accurate credit report.”

Onstage, Liistro and Eric Kamerath, the legal counsel for Utah-based Lexington Law, the largest credit-repair company in the United States, delivered CreditCon’s legislative update. They gave a quick rundown of proposed bills in various states that, among other things, would require credit-repair agents and businesses to identify themselves when filing dispute letters with debt-collection agencies on behalf of clients. The lobbying effort is worth it for the $20 billion debt collection industry: Federal law allows debt collectors to ignore letters from credit-repair organizations, so debt collectors who can disregard millions of letters are more likely to collect. This is why credit-repair companies generally try to avoid giving any clue that their dispute letters were written by someone other than the debt’s owner. (A recent congressional investigation found that the credit bureaus have examined envelope characteristics, ink color and fonts, as well as the language being used, in order to identify letters from agents.)

Kamerath and Liistro went on to describe their industry’s lobbying battles. Liistro recounted an exchange with an executive at an Illinois-based nonprofit, Working Credit NFP, which has received funding from the credit-card industry and had lobbied for a bill in Illinois to restrict credit repair. She told him they “had every intention of shutting down credit repair,” he said. “And I know this because they told me so to my face, right after they said: ‘You seem like a nice guy. But what you do is evil, and you need to get a new job.’ They’re very adamantly against credit repair.”

Such lobbying war stories were relatively minor concerns compared with what Kamerath was leaving unsaid. His company’s biggest existential threat was coming from federal regulators. In May 2019, the Consumer Financial Protection Bureau sued Lexington Law in federal court for charging upfront fees for its credit-repair services. Those fees, it claimed, were substantial: as much as $3.1 billion in gross revenues since about 2016. Earlier this year, the C.F.P.B. submitted a request to the court that Lexington Law pay those fees back to consumers. While attending CreditCon, Kamerath had approved a response to that request, explaining why it would be impossible. His company’s “financial resources are dwindling and nearing zero,” it read.

When I visited Liistro at his company headquarters in Mobile after CreditCon, he told me that he was doing less actual credit repair these days. He found it more profitable to sell his software package, Credit Admiral, which credit-repair agents use to run their business and generate dispute letters. He had fewer than 50 credit-repair customers these days and claimed to be owed more than half a million dollars in unpaid fees. Though he did so rarely, he said, he sometimes hired a collection company to go after those debts — “who will then report it to the credit bureaus, coincidentally.”

The injustices of America’s credit system have not gone entirely unnoticed by national politicians in recent years. During his presidential campaign for the Democratic nomination in 2019, Bernie Sanders proposed a public credit registry, housed within the C.F.P.B., to replace the for-profit system, along with a ban on the use of credit checks by nonlenders, including landlords, employers and insurers. But the idea gained little traction. President Biden — whose largest campaign contributors before joining Barack Obama’s presidential run in 2008 included the employees of a credit-card company — also suggested the idea of a public registry during his last campaign.

America’s current system is itself a product of a previous reform effort. Into the early 1960s, the public was largely oblivious to the power of what were then well over a thousand credit bureaus, which mostly operated regionally. “I am constantly amazed at the average person’s complete lack of understanding of the functions of a credit bureau,” David Blair, a professional credit manager and advocate for the credit bureaus, wrote in a trade journal in 1954. “There is, in my opinion, no organization that affects the daily lives of so many people that is so little understood.” That ignorance ended as computer databases supercharged the industry’s surveillance powers. What had been a fragmented and paper-based industry quickly was consolidating and tracking intimate details — sexual orientation, marital status, even cleanliness. Mistakes were rampant and resulted in congressional hearings by 1968, when the credit bureaus faced their first major existential threat: a proposal for a government-managed registry that would replace the for-profit system.

If there’s an origin story for credit repair, it can be traced to those hearings. To avoid a crackdown, and their own obsolescence, the bureaus compromised: For the first time, they issued guidelines for how people could correct errors on their credit reports. Two years later, consumers were granted the “right” to fix errors on their report in a sweeping law, the Fair Credit Reporting Act, to this day the most comprehensive legislation regulating the behavior of the credit bureaus. Individuals, in effect, were made quality-control agents of what would grow into a billion-dollar industry. The act also required the bureaus to follow “reasonable procedures to assure maximum possible accuracy of information.”

The unresolved balance between the “right” of individuals to identify errors and the bureaus’ obligation to ensure accuracy helped create space for the credit-repair industry to thrive. What became known as “credit-repair clinics” proliferated into the early 1980s, when the American economy was undergoing transformative change. Wages flatlined and consumer debt soared, as credit cards became an increasingly easy way to pay for things. But as low-income households were denied cards, newspaper classifieds were soon dominated by credit clinic ads promising “New Credit in 24Hr” or “CREDIT $10: Get VISA/MC.”

By 1993, the bureaus were struggling with the deluge of dispute letters and the costs of managing them. Together, the bureaus established e-Oscar, or the Online Solution for Complete and Accurate Reporting, which passes such complaints to the original creditors — a bank, say, or credit-card issuer — to verify or investigate. It automated the dispute process, and much like medical-insurance billing, the system came to run on over two dozen codes: 024 for “claims account closed by consumer”; 019 for “included in the bankruptcy of another person”; 002 for “belongs to another individual with the same/similar name”; and so on.

Automation didn’t dampen dispute volume; rather, it kept rising, and the bureaus lobbied Congress for relief. In 1996, the Credit Repair Organizations Act banned upfront fees on the grounds that they “worked a financial hardship upon consumers, particularly those of limited economic means and who are inexperienced in credit matters.” Perhaps most consequential, the law defined, at last, what a credit-repair organization was: a person who sells, promises or performs a service for the purpose of improving a consumer’s credit record, history or rating.

That definition would become a problem for the bureaus when they found a lucrative new product line for themselves: credit-monitoring services. Equifax started selling products like “Credit Watch Gold” and “Score Watch” — and then faced suits for violating a law the credit bureaus had lobbied to pass because it charged upfront fees. The new legal definition of credit repair was being “misread to cover credit-monitoring products,” Robin Holland, then senior vice president of global operations at Equifax, testified during hearings in 2007. All three bureaus sell credit-monitoring products today. More recently, as demand to “improve” credit records has intensified, Experian has been using the marketing pitch “Increase Your Credit Score Instantly” to promote its credit-score-tracking app, Experian Boost, which was introduced in 2019.

Even as the automation of the dispute system cut costs for the bureaus, it also made running a national credit-repair company easier. In 2013, Daniel Rosen started Credit Repair Cloud, after a bank error ruined his credit, he has claimed. C.R.C.’s software, which sells for about $180 a month, comes with a database of dispute letters. From his headquarters, on Venice Boulevard, he produces a steady stream of promotional content: “Delete Negative Items from Credit Reports INSTANTLY With This Easy Trick!” “Late Payment Removal Strategy: Boost Credit Scores up to 192 Points! Strike Back Against Debt Collectors and Win!” Rosen claims on his website that his company’s users have earned $197 million. Rosen avoided legal scrutiny for years because he wasn’t selling credit services directly to consumers. But in September 2021, the C.F.P.B. sued Rosen for encouraging “credit-repair businesses to charge illegal advance fees.”

Citing the demographics of C.R.C.’s customers — 80 percent were “people of color,” and 60 percent were women, many of whom were single mothers who have been homeless in their lives — lawyers for Rosen, a white man, asked the judge to dismiss the lawsuit because it threatened the livelihoods of C.R.C.’s users. (According to court filings, few C.R.C. users make much money; 68 percent make less than $24,000.)

Rosen was right that his platform has become indispensable for small credit-repair businesses, including Taqwanna Clark’s. What’s less clear is whether the software puts such small operators in a position to succeed, given the fees they pay for it and the difficulty of attracting clients in a highly fragmented market. In 2020, Teaunna Wilson, a mother of five in Durham, N.C., took out a subscription to Credit Repair Cloud. She had started her credit-repair business to supplement her hourly wages from working at a call center. She spent the last of her stimulus checks to establish her brand: KB’s Way Credit. “I had all the bells and whistles and didn’t have the clientele to pay for it,” she told me. Some months she made $500, some nothing at all. Her free initial online meetings with customers frequently turned into therapy sessions. “There’s so many women like me,” she told me. “They’re single mothers, or they’ve been in a relationship, and they lost their way.” After a trip to the post office — where she spent $240 sending off dispute letters by certified mail for clients — she realized more money was going out than in. “I had a hard time finding a healthy balance between being helpful and being profitable,” she says.

As the C.R.C. case moved through the courts, Rosen openly taunted the C.F.P.B. on social media. He successfully demanded a jury trial, which was originally scheduled to start in late May. (Rosen declined to comment for this article.) In late February, the C.F.P.B. faced a legal challenge of its own. The Supreme Court announced it would review a lower court’s case that questioned the constitutionality of its funding stream. (Its budget is transferred directly from the Federal Reserve and does not require congressional approval; in fiscal year 2022, the agency spent $622 million.) A ruling on that case isn’t expected until 2024. Citing the case, Rosen’s lawyers requested and received a stay.

“I love myself,” was the call. “I love myself,” the response. At a craft brewery in Atlanta, this wasn’t church, but it felt a little like it. Presiding from an elevated platform, Umar Clark (no relation to Taqwanna) punctuated his spiritual call-and-response with questions of a more practical, worldly nature: “When you got that credit card, did you understand what you were getting into?” To the people in the audience, lured by Instagram posts to this “Do for Self Weekend” gathering, the promise on offer was escape: from the stigma of bad credit and the harassment of debt collectors — if they embraced Clark’s mission to “Bankrupt the Bureaus,” which also happened to be the title of his self-published book.

Onstage, Clark, whose popularity exploded during the early days of the pandemic, wore dark sunglasses, a red bow tie, a white Oxford shirt and a dark suit, and he told his mostly Black audience, repeatedly, “Credit is your life.”

He channeled his disdain for the credit bureaus on Instagram and found a reservoir of discontent, churning out a steady stream of posts to his more than 63,000 followers, ranging from the comedic — the metaphorical deployment of Vaseline in preparation for a quarrel with a debt collector — to the elaborately produced. In one, Clark rides in the back of a Rolls-Royce driving to the midtown Atlanta headquarters of Equifax. Arriving at its glass-and-steel building, he stares with a mix of bravado and triumph. Later, he will tweet: “Families broken up, suicides and trauma. All because we were never taught that credit reporting was voluntary. People literally killing themselves over made up credit scores.” On radio shows and in social media posts, he repeatedly questions the power of debt collectors: “They’re not supposed to harass you, but there’s no law that says you can’t harass them.” And the bureaus: “If I rob a bank, they report it to the FBI/The Government. A bank robs me, and they report it to Transunion, Equifax and Experian.”

It wasn’t until 1976 — more than a full decade after the landmark Civil Rights Act — that explicit racism in credit decisions was deemed illegal. Until then, discriminatory practices in lending had not been uncommon and created what Josh Lauer, a media historian and associate professor of communication at the University of New Hampshire, has called a “white credit economy”; Mehrsa Baradaran, a law professor at the University of California, Irvine, has referred to a system of “Jim Crow credit.” To comply with the Equal Credit Opportunity Act, the credit bureaus stopped using categories like gender and marital status and instead claimed to rate people on individual behavior. This legal fix, while officially outlawing racism and sexism in the credit system, helped give birth to a new financial world in which the spiraling consequences of bad credit for individuals could go on without end. Firms in the banking, insurance and credit-card industries could now charge different prices to different people according to a person’s credit. Such practices, known broadly as risk-based pricing, unleashed far-reaching economic damage within the Black community. Fourcade and Healy, the sociologists, have written that “the idea that the poor ought to qualify for more favorable terms because they were poor was gradually replaced by the idea — now almost completely taken for granted — that the terms of credit ought to depend solely on one’s prior credit-related behavior.”

‘Cleaning Experian and Equifax is small. You got to clean your spirit now. That’s the real consumer report.’

In a recent study using a national survey and interviews, Davon Norris, a research fellow in organizational studies at the University of Michigan, sought to understand people’s experience of credit, debt and how they engage with their credit score. Black respondents, he found, “feel their credit score exacts a significant psychological tax,” with higher levels of anxiety, stress and feelings that their score is a controlling factor in their life. White respondents were largely unaffected by their credit scores.

At the Atlanta retreat, Clark shared a stage with Asma AlFatihi, known on Instagram as the Original Consumer Protection Goddess. Her handle is creditrepairfraud2.0, and her website’s bio once claimed that AlFatihi “has been called ‘Harriet Tubman’ for a reason. She is a chosen vessel to free the minds of the people via consumer laws.” In her self-published book, “Credit Repair Fraud,” written under one of her pseudonyms, Shaquan Envi, in May 2021, she railed against the credit-repair industry: “They make it seem as if there is some secret sauce and they are the only ones that know. It’s time up for fraud amongst our people.” AlFatihi tells her followers to “study, study, study.” And they do, examining statutes and legal texts like first-year law students.

Clark instructs his followers to write their own dispute letters, file affidavits, issue demand letters to creditors — upending the passive model that has defined the credit-repair industry for decades. It’s a message mixed, at times, with more spiritual commands. “There’s no success if you don’t love yourself,” Clark told a YouTube radio host last year. “There’s none. You just a robot sending out dispute letters all day. Cleaning Experian and Equifax is small. You got to clean your spirit now. That’s the real consumer report.”

“So let me tell you something deep,” Clark told his audience. “You can’t just blame them … you got to think for yourself.”

“I love myself,” Clark said.

“I love myself,” the crowd roared back.

After two years in credit repair, Taqwanna Clark still has to work full-time weekend shifts as a government security guard. She puts every dollar in revenue from credit repair back into the business. In late April, she spent $1,500 on travel and for admission to CreditCon in New Orleans. When she returned to Houston, various annual bills were waiting for her. She detailed them to me over the phone: Credit Repair Cloud software, $1,831; Zapier, a program that helped her stay in touch with customers, $239.88; Squarespace, to set client meetings, $324; Billsby, subscription billing software, $420; Dropbox, to securely store client documents, $319.67: ActiveCampaign, for mailers, $588 annually. There is also the cost of envelopes, printer ink and certified mail when sending client letters.

“I’m not turning a profit at all,” she told me. Clark estimated that 60 or 70 active clients would be needed to change that.

To bring in traffic and prospects, she figured she had to be more active on social media. It was the part of her work she hated the most. She recently interviewed someone to do that job for her, but the charge was steep: $800 per post. “The people that are making millions, what I noticed about them, their social media campaign marketing is elite,” she says. “Either they have a really compelling, amazing storytelling skills, or they can write a freaking post on Facebook that are making you feel like you were there.” Clark’s personal Instagram, where she also promotes her services, has only 2,630 followers, the Credit Lift account only 65. “Right now,” she adds, “I’m not in that space at all.”

Recruiting clients, especially around Houston, was complicated by a video of Roekeicha Brisby, owner of Rose Credit Repair, being led away in handcuffs, that played on the local news last summer. Brisby was charged with committing fraud and forgery in excess of $3.3 million that allegedly involved falsifying and filing identify-theft reports with the police, to be used as documentation when sending dispute letters to the bureaus. (The case is still pending an independent investigation, and a court date has been set for later this year.) Such “credit sweeps” erased problematic tradelines. One prospective client demanded that Clark visit her home before she signed a contract. “I was so kind of blinded and clouded by trying to prove to her that I wasn’t scamming,” she says.

But she was trying to follow closely the laws regulating the industry. Referring to the C.F.P.B. and the F.T.C., she says, “I don’t want none of those acronyms knocking at my door.” While a social media competitor like boostmyscoresnow might offer quick fixes — “800+ Scores in 7-10 Days!” — Clark tempered her social media posts. She emphasized her measured approach: “How long does credit restoration take? Initial disputes: 45 to 60 days. Overall: three to six months.” In late May, she lost a potential new client as a result. A co-worker was losing her apartment and, anxious that another landlord wouldn’t rent to her with her bad credit, asked Clark about doing a credit sweep. “It was just understandable desperation,” Clark says. “When people are in a situation where they have to move in 30 days, they are willing to do whatever they can do to get out of their situation quickly, to pay whatever they have to.”

Despite the difficulties, Clark still sees her work as a mission, not just for her clients but for her own family. She wanted to change a generational pattern, to avoid going through anything like a foreclosure, as her mother had. Clark didn’t blame her for her ending up with bad credit at such a young age. “I don’t believe that she knew, or that anyone taught her,” she told me. Clark wanted her daughter to avoid the mistakes of her mother and grandmother. “You’re not going to be out here ignorant,” she told her daughter. Thanks to Clark’s intimate knowledge of the system, she went off to college last fall with credit scores hovering around 800.

Mya Frazier is a journalist in Ohio who reports on the power of the finance and credit industries. Her last article for the magazine, on the role of the punitive credit-reporting system in America’s housing crisis, was recognized by the National Press Foundation with a Poverty and Inequality Award.

A version of this article appears in print on June 11, 2023, Page 28 of the Sunday Magazine with the headline: The High Cost of Bad Credit Scores.